The Baseline Manipulation is Real and Material; Pre-Revaluation Value Adjustment and Assessment Timing Question; Roy Carroll Edition

The Discrepancy vs. Peers is Striking

A valuation change for Center Pointe Unit 1603 at 201 North Elm Street to be voted on by Guilford County Commissioners tonight shows a notable downward adjustment for a major political campaign contributor and property owner relative to the county’s 2026 mass revaluation.

It’s buried in Item 3 of “Miscellaneous” on the Consent Agenda;

https://guilford.legistar.com/Calendar.aspx

Which includes amongst other properties owned by the same company;

On March 4, 2026, the assessed value of the unit, owned by Park View Development, LLC, otherwise known as Roy Carroll for 2025 was reduced from approximately $322,200 to $285,300;

Realtor.com estimates the property could sell for $388,000.

Original 2025 value; $322,200

Adjusted 2025 value (as of 3/4/2026); $285,300

2026 revaluation; $364,100

The timing raises the question of whether valuation adjustments are being applied differently for a connected few.

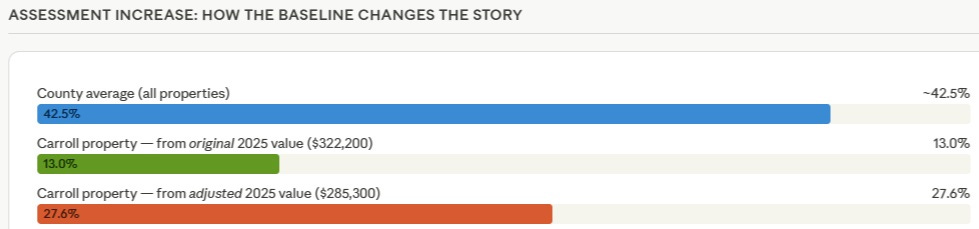

The reduction means the property’s post-revaluation increase will look less significantly lower than the countywide average of ~42.5%;

From the adjusted value; $285,300 → $364,100 = +27.6%

From the original pre-adjustment reality; $322,200 → $364,100 = +13.0%

The county average increase (~42.5%) is supposed to be based on true prior values, not backdated lowered appeal-adjusted numbers;

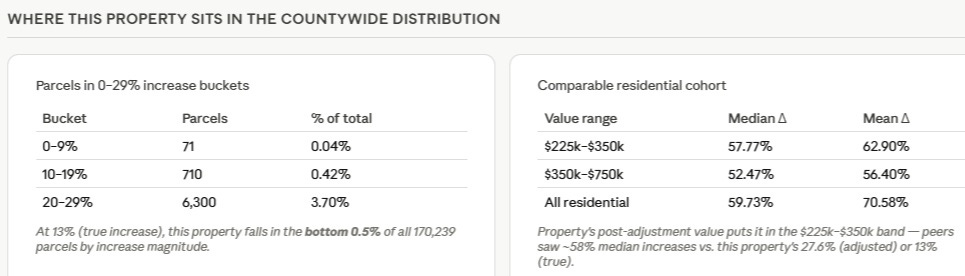

True increase for Roy Carroll’s property = ~13%

County average: ~42.5%

On this property, Mr. Carroll is a much bigger winner under revenue neutral;

Estimated tax cut: ~$880/year from $4,259.53 to ≈ $3,378

Reduction: ~20.7%

After the County’s reduction, the math looks like Carroll +27.6% would imply;

Only a ~10.5% tax reduction (~$440 savings)

The core issue is a baseline manipulation problem. When Roy got his condo retroactively reduced within the revaluation reset, it looks like he’s disproportionately benefiting with some help.

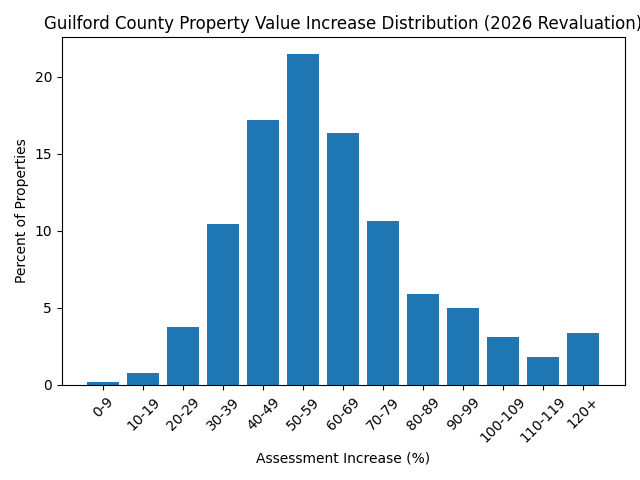

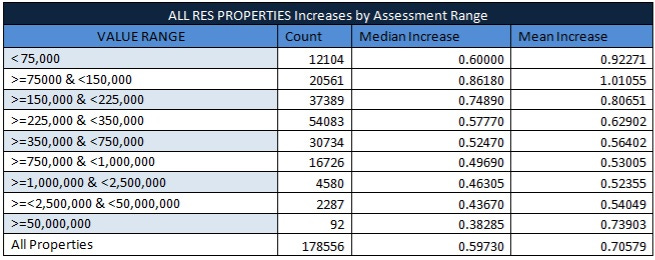

Meanwhile, Guilford County’s residential properties rose to a median increase of 59.73%;

The $225,000 & <$350,000 value range produced a median increase of about 58%, but Carroll’s only went up 13% from where it was revalued on March 4th;

The 27.6% increase is still below average, but much less conspicuously so. The backdated reduction delivers a double advantage; it lowered the 2025 tax bill itself (from $322,200 to $285,300 base) and resets the measurement baseline for 2026, making a $364,100 revaluation appear as a 27.6% jump rather than 13%, which is the opposite of what happened for most homeowners. Roy Carroll’s condo went up within the one percent of all county parcels;

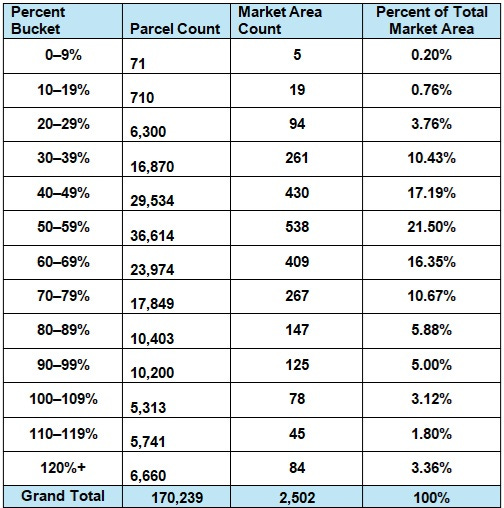

Another way to look at it, provided by Guilford County;

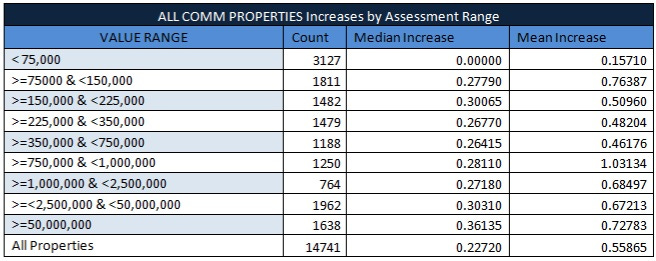

Commercial properties saw a lower 22.72% increase, which will have to be made up for by lower tier residential;

Who would have thought?

The data does not support an innocent explanation. The vast majority of properties saw much larger percentage increases. The retroactive baseline change is a textbook example of manipulating the measurement period to disguise a windfall.

The question is whether a system that allows a connected owner to retroactively lower his prior year’s assessment after seeing the new revaluation is procedurally fair to the other 170,000+ property owners who had no such opportunity.

Related;

Thanks for reading Public Integrity Watch! Subscribe for free to receive new posts and support my work.