$2 BILLION AND MELVIN “SKIP” ALSTON; FORMAL ETHICS, RECUSAL, TRANSPARENCY, AND PROCEDURAL DUE PROCESS COMPLAINT REGARDING GUILFORD COUNTY, NC COMMISSIONER CHAIRMAN

County leaders emphasized lower tax rates while school construction borrowing depends on dramatically higher property tax collections.

Complainant;

George Hartzman

Public Integrity Watch

Respondent;

Melvin “Skip” Alston

Chairman, Guilford County Board of Commissioners

Summary of Complaint

The central concern raised by this complaint is whether Guilford County provided taxpayers with meaningful transparency and meaningful notice regarding;

the true scale of proposed FY2026-27 reassessment property tax increases;

and the extent to which the proposed budget depends upon dramatically increased real estate reassessment driven revenues to support $2 billion more debt that many county taxpayers may not fully understand.

This complaint also concerns Chairman Alston’s participation in misleading revaluation budget presentations while Guilford County proposed dramatic increases in property taxes while publicly emphasizing reduced nominal tax rates and “revenue-neutral” messaging that did not clearly communicate the true scale of the proposed property tax increases.

This complaint further concerns substantial appearance of impropriety, associational conflict, transparency and public trust concerns arising from Chairman Melvin “Skip” Alston’s overlapping leadership relationships involving;

Guilford County appropriations,

Guilford County Schools governance,

Continuum of Care governance structures,

and politically connected institutional networks.

Relevant Facts

Publicly documented information establishes the following;

Melvin “Skip” Alston is the Chairman of Guilford County’s Board of Commissioners.

Deena Hayes-Greene is the Chair of Guilford County Schools, which receives budget appropriations from Guilford County, voted for by Alston.

Skip” Alston is a Realtor, real estate developer, and leader of Alston Realty Group

Deena Hayes-Greene’s husband, John Greene, is President/CEO of a certified Minority and Women Business Enterprise (MWBE) and Historically Underutilized Business (HUB) construction firm.

Deena Hayes-Greene and John Greene are co-founders of Black Wall Street LLC, involving economic development, redevelopment, housing and neighborhood revitalization. The firm employs a lending specialist and a real estate broker.

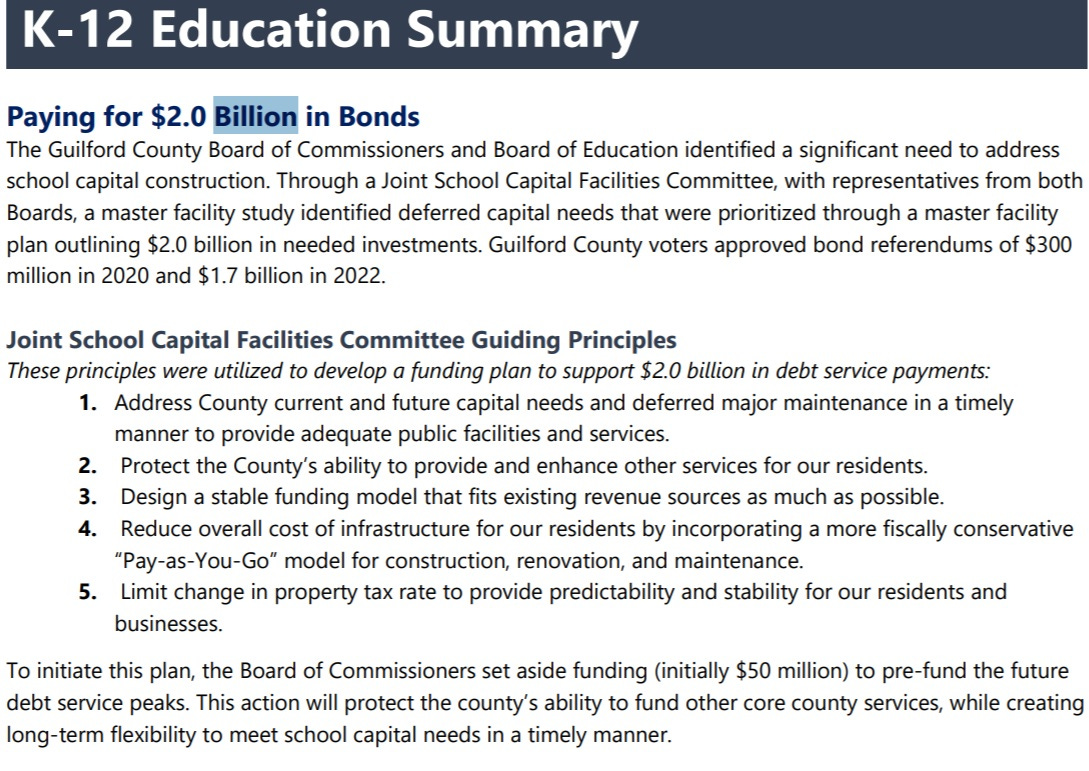

Guilford County voters approved $300 million in school construction bonds in 2020, and $1.7 billion in 2022, for a combined $2.0 billion school capital program.

Skip Alston wants to raise property taxes 19% to borrow $2 Billion using the 2026 reassessment to fund school construction debt after voters rejected proposed sales tax funding in 2020 and 2022 without widespread public disclosure/knowledge.

$2 billion in school construction bond obligations could cost taxpayers in excess of $3 billion over time once long-term interest costs are included.

Guilford County is the lead agency for the Continuum of Care (COC) homelessness governance system, which coordinates with housing and homelessness programs involving municipal, nonprofit, and non-governmental organizations.

Deena Hayes-Greene is publicly identified as co-founder/managing director of the Racial Equity Institute (REI).

Guilford County’s Continuum of Care Member Portal says “The Partnership Project is working with the Racial Equity Institute to provide a series of trainings in Greensboro.”

The International Civil Rights Center & Museum (ICRCM) will receive about $4 million in combined direct governmental support from the City of Greensboro and Guilford County property tax increases produced as a result of the County’s 2022 revaluation.

Deena Hayes-Greene is Co-Chair of the Board of the ICRCM with Skip Alston.

Skip Alston and Deena Hayes-Greene are leadership figures within the Guilford County Black Caucus and both are reportedly members of the Simkins Political Action Committee (PAC).

The proposed budget explicitly states the County developed “a funding plan to support $2.0 billion in debt service payments” “to address school capital construction”. It also says one guiding principle was to “Design a stable funding model that fits existing revenue sources as much as possible.”

Guilford County’s Budget Message doesn’t mention the $2 billion.

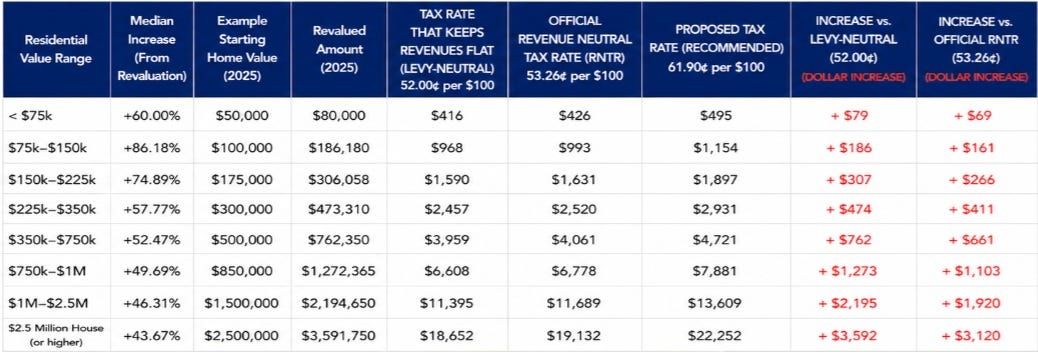

Revaluation-Era Property Tax Increase Transparency Concerns

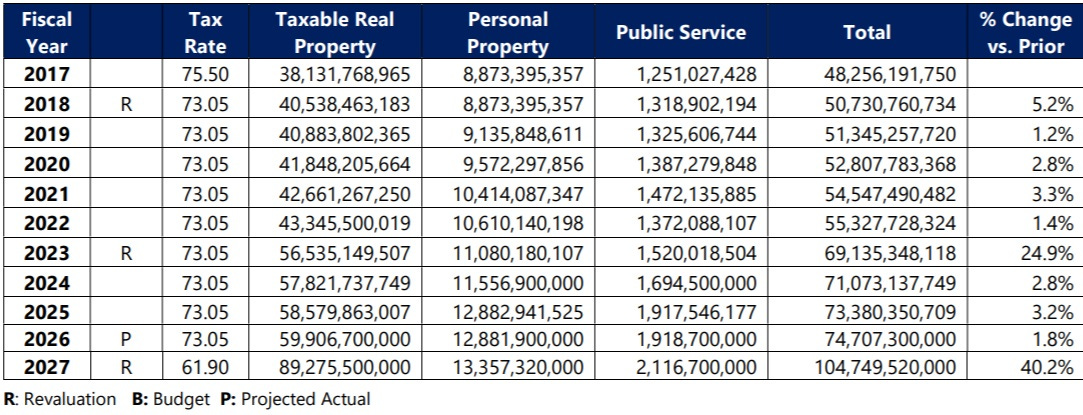

Guilford County publicly characterized the FY2023 proposed budget as a “15% budget increase,” while property taxes increased roughly 25% following the 2022 revaluation without sufficient transparency. Skip Alston was Chairman of the County Commissioners;

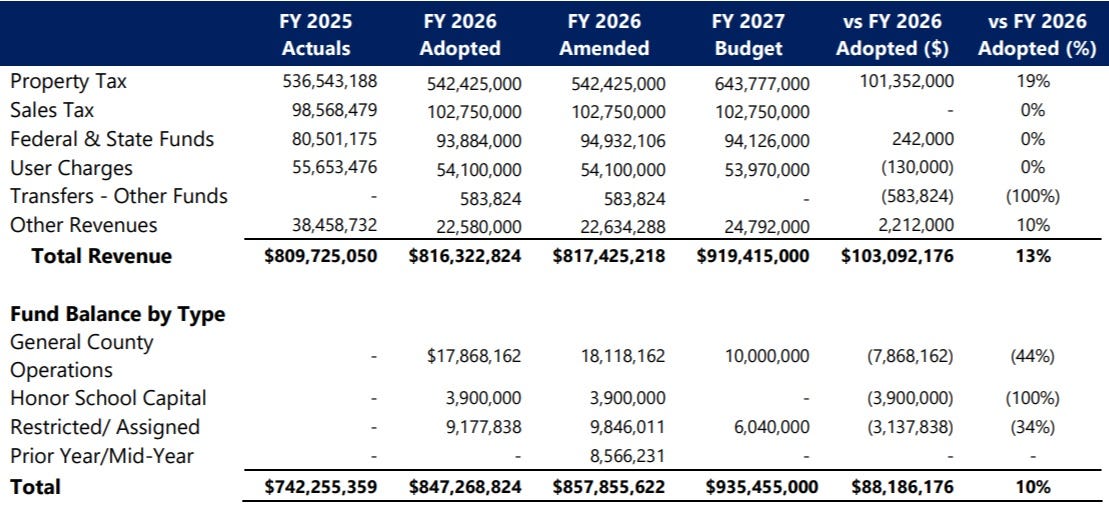

Guilford County characterized the FY2027 proposal as a 10% budget increase, but not unlike 2023, property taxes increase 19% without proper disclosure;

The County’s public presentations of the FY2023 and FY2027 proposals as 15% and 10% increases materially understated the practical scale of the reassessment-era property tax increases of 25% and 19% without making it clear.

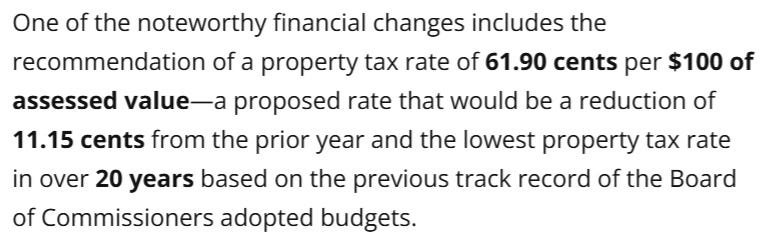

At the same time, the County emphasized the “lowest tax rate in 20 years,” and that the proposal was only “8.64 cents above revenue neutral”, and statements regarding historically low tax rates without making the actual impact publicly known.

Those public representations did not clearly communicate;

the actual increase in total property tax collections,

the distinction between exact levy-neutral calculations and statutorily adjusted “revenue-neutral” calculations,

or the extent to which Guilford County’s proposed spending plans depended upon approximately a 19% increase in reassessment-driven property tax revenues above prior-year collection levels.

The County’s public presentation and related press materials emphasized the proposed tax rate represents an “11.15 cent reduction” and characterized the proposal as fiscally restrained while simultaneously downplaying or obscuring the actual impact of massive tax increases on low income taxpayers without telling anyone.

The County’s messaging created the misleading impression taxpayers are broadly receiving tax relief because the nominal tax rate is lower.

ABC45’s Christian Gladney repeated Guilford County’s deceptive talking points;

Victor Isler, who serves as the county manager, outlined the details of this $935 million proposed spending plan—an increase of approximately 10.4% in comparison to last year’s finalized budget.

Without mentioning the 19% property tax hike.

And the same misleading narrative;

Alston failed to adequately have the County disclose several critical facts necessary for the public and press to understand the true financial impact of the proposal, not unlike 2022.

The County’s messaging relies heavily on the statutory “revenue-neutral” calculation while failing to explain that the state-prescribed formula is not the same as exact levy neutrality.

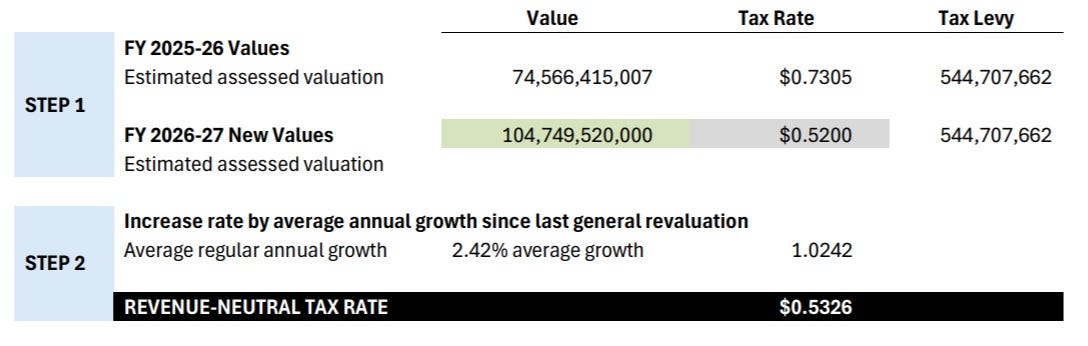

From Guilford County’s proposed 26-27 budget document;

A rate materially lower than 53.26 cents ($13 million) would be required to reproduce the prior year’s actual property tax levy.

Yet, from the County’s presentation;

The County’s repeated public framing obscures this distinction and materially misleads taxpayers regarding the scale of the proposed increase, relatively a repeat of the 2022 revaluation and subsequent budget.

52¢ was the rate that actually kept revenues flat after revaluation.

“This recommendation is 8.64 cents above that level because responsiveness and quality service delivery does not maintain itself,” Isler said before the Commission

The County then applied a built-in 2.42% “historical growth” adjustment, which increased the official statutory “Revenue Neutral Tax Rate” (RNTR) to; 53.26¢.

61.9¢ - 52¢ = 9.9¢, not 8.64

53.26¢ ≈ $13.2 million in additional property tax collections before the ‘proposed’ $89.3 million.

Official communications repeatedly emphasized the “8.64 cents above revenue neutral” figure while failing to clearly explain the statutory RNTR already contains an additional built-in tax hike above true levy neutrality.

Materially misleading;

All before the 8.64 cent increase.

The reassessed tax base already incorporated substantial growth-related increases, including many physical and taxable value changes associated with;

new construction,

improvements,

discoveries,

and other additions to the tax base since the 2022 revaluation;

The County’s statutory “revenue-neutral” calculation still applied an additional growth adjustment after reassessment.

The formula effectively layered an additional growth related assumption on top of a reassessed base that had already absorbed much of the same growth through the revaluation process itself, which the County didn’t properly disclose.

Functionally, taxpayers could reasonably perceive that growth was recognized twice;

first through the reassessment and expansion of the taxable base itself;

and again through the statutory “revenue-neutral” growth adjustment factor.

The County’s published “revenue-neutral” rate therefore embedded approximately $13.2 million in additional property tax above exact levy neutrality before the 'proposed tax increase’ was proposed.

Chairman Alston’s County publicly characterized the adjusted figure as “revenue neutral” without clearly explaining;

the distinction between exact levy neutrality and the statutorily adjusted figure;

the extent to which reassessment had already substantially expanded the tax base;

or that the published “revenue-neutral” rate already incorporated millions of dollars in additional collections above exact neutrality.

The Chairman failed to explain the redistributive effects of reassessment. Properties that increased more than average would shoulder a larger share of the tax burden. Skip repeatedly omitted these crucial facts.

The 2026 revaluation created a regressive tax on lower valued properties which the County failed to disclose. Even under the proposed “lower” tax rate, lower-value homes show some of the highest percentage increases in total tax burden.

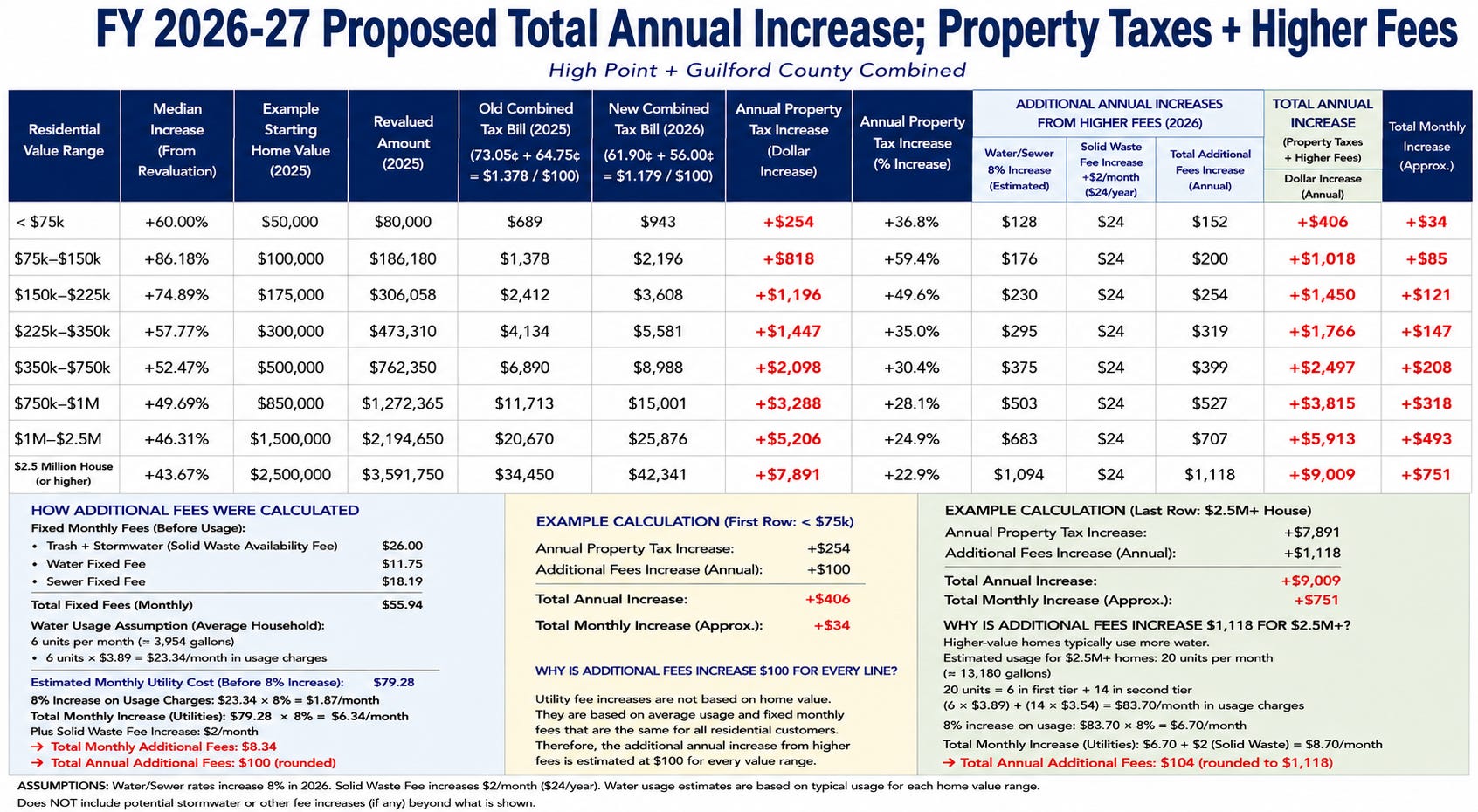

Guilford County and the City of High Point’s combined proposed budget impacts;

Cyril Jefferson is the Mayor of High Point, North Carolina. Publicly documented materials place High Point Mayor Cyril Jefferson within overlapping city governance, homelessness governance, Guilford County Black Caucus leadership, and Simkins PAC political endorsement networks connected to many of the same county, city, nonprofit and institutional leadership figures involved in FY 2026-7 reassessment budget and appropriations decisions.

Many lower income residents are likely to experience the effects of substantial tax increases despite the misleading lower nominal rate.

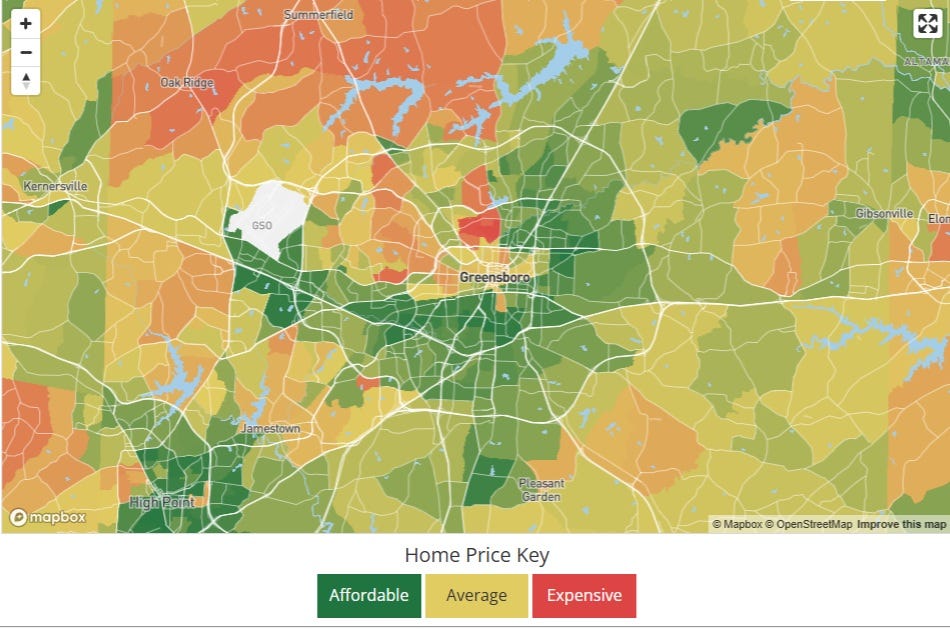

Here’s who’s going to pay more than less, and vice versa;

Affordable = Green = The lowest income and real estate valued areas

If the City of Greensboro raises taxes as much as Guilford County wants to;

Government officials have an obligation to provide clear, transparent, and non-misleading financial information to residents and the press, particularly regarding taxation. While technically accurate statements can still be materially misleading through omission, framing, or selective presentation of facts, public trust depends on honest and complete disclosure.

Alston’s repeated messaging mislead residents into believing;

the county is reducing taxes overall;

most taxpayers will experience lower tax bills;

“revenue-neutral tax rate” (RNTR) means the same revenue; and

the proposed budget represents only minimal growth.

These impressions are inconsistent with the actual financial effects of the proposal, which has been repeated by Greensboro’s News & Record;

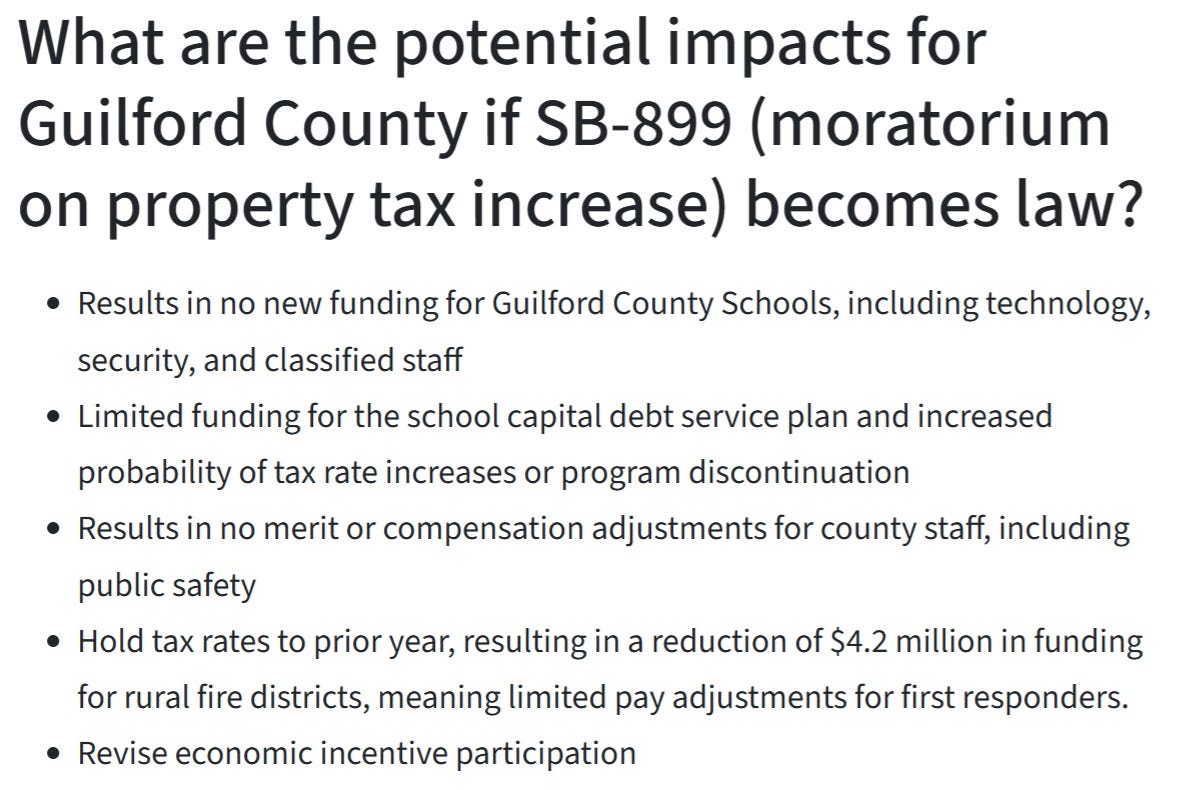

The County’s Budget page says “Guilford County has developed an alternate recommended budget if property tax assessments are paused for a year.”

The County warned that limiting reassessment-era property tax increases could result in:

reduced school funding,

limited debt-service funding for the school capital plan,

elimination of compensation increases for County employees and public safety personnel,

reductions in rural fire district funding,

and revisions to economic development participation;

Reasonable taxpayers could conclude, absent the presentation structure and messaging framework, public resistance to the magnitude of the reassessment-era increase may have been substantially greater, hence the shift to a different budget if the revaluation moratorium goes into effect.

Additional Public Statements by Chairman Alston

On May 14, 2026, Chairman Alston publicly acknowledged that the County’s proposed FY2027 budget was fundamentally built around increased reassessment-driven revenues.

The Rhino Times’ Scott Yost quotes Chairman Alston as stating “Victor Isler’s proposed budget currently assumes revenue based on the new revaluation numbers…”

Chairman Alston further warned that if state legislation delayed implementation of the reassessment increases;

Guilford County would likely need to cut services,

reduce staffing requests,

limit school funding,

and substantially rethink the proposed budget.

The contrast between public facing messaging minimizing the appearance of the increase, and public admissions that major spending plans depended upon dramatically expanded reassessment-driven revenue without revealing the details, raises substantial transparency and public trust concerns.

The statements substantially undermine repeated emphasis on reduced nominal tax rates and “revenue-neutral” framing, because County leadership openly recognized and materially reinforced that the proposed budget presentation strategy relied on the public not understanding what they should.

Applicable Guilford County Ethics Standards

The Guilford County Board of Commissioners Code of Ethics, signed by Chairman Alston as Chairman of the Board, expressly requires commissioners to;

avoid impropriety,

avoid conduct creating the appearance of impropriety,

act with integrity and independence,

preserve public confidence in government,

and conduct governmental affairs openly and transparently.

The Ethics Code specifically states;

“Board members should avoid impropriety in the exercise of their official duties.

Their official actions should be above reproach.”

The Code further provides;

“A board member is considered to be acting with impropriety if a reasonable person who was made aware of the totality of the circumstances surrounding the board member’s action would conclude that it was more likely than not that the behavior did not befit someone in the board member’s position.”

Importantly, the Ethics Code also expressly recognizes that;

“close familial, business, or other associational relationship[s]” may create conflicts serious enough to invalidate governmental actions in certain contexts.

Basis for Complaint

The publicly promoted “revenue-neutral” figure was materially higher than the exact levy-neutral rate required to reproduce the prior year’s property tax levy.

Reasonable taxpayers could therefore have understood the County’s public messaging to imply proposed reassessment-era tax rates were substantially closer to neutral than they actually were in practical fiscal effect.

County budget figures demonstrate;

the 2022 reassessment cycle produced approximately a 25% increase in total property tax collections,

while the proposed FY2027 budget reflects 19% property tax hike.

Despite this, government outreach continued emphasizing;

reduced nominal tax rates,

“lowest tax rate in 20 years” language,

and comparisons against statutorily adjusted “revenue-neutral” figures,

without equally prominent disclosure regarding the resulting increase in total collections and taxpayer burden.

These concerns were materially reinforced by Chairman Alston’s own public statements.

On May 14, 2026, Chairman Alston publicly acknowledged the proposed FY2027 budget was fundamentally dependent upon revenues generated by reassessment increases,

and that without those reassessment-driven revenues the County would likely need to;

reduce staffing requests,

cut or limit services,

reduce school funding,

and substantially revise the proposed budget.

Skip Alston’s statements confirm Guilford County’s proposed spending levels depended upon a misleading portrayal of dramatically expanded reassessment-driven revenues beyond exact levy neutrality.

Meaningful public participation and procedural fairness require taxpayers to reasonably understand;

the actual fiscal impact of proposals,

the magnitude of resulting collection increases,

the distinction between exact levy-neutral and statutorily adjusted “revenue-neutral” calculations,

and the extent to which proposed budgets rely upon reassessment-driven revenue expansion.

For the FY2027 budget process, Guilford County held or scheduled 5 Budget sessions across the county in April 2026, and none of the ‘actual’ information was presented to the public.

When official governmental messaging emphasizes;

reduced nominal tax rates,

and “revenue-neutral” framing,

while minimizing or failing to clearly disclose dramatic increases in total collections and taxpayer burden, taxpayers were deprived of meaningful notice necessary for informed public participation, informed challenge and procedural fairness.

These concerns implicate;

the Guilford County Code of Ethics,

principles of governmental transparency,

and procedural due process protections under the 14th Amendment to the United States Constitution.

The concern is not merely personal friendship or political association, but that Chairman Alston simultaneously occupies leadership roles in organizations receiving county appropriations, participates in funding decisions involving systems connected to overlapping leadership networks, votes on appropriations benefiting Guilford County Schools chaired by Deena Hayes-Greene, and participates in County governance structures connected to Continuum of Care systems publicly promoting taxpayer funded REI-associated initiatives led by Hayes-Greene.

The totality of these overlapping relationships and public representations creates substantial appearance-of-impropriety concerns under the County’s own adopted ethics standards.

Reasonable members of the public could conclude that Chairman Alston’s reassessment tax increase proposals were not clearly communicated to the public in plain terms.

Procedural Due Process and Public Notice Concerns

This complaint additionally raises concerns regarding meaningful public notice and procedural fairness under the 14th Amendment to the United States Constitution.

Meaningful public participation depends upon taxpayers being able to reasonably understand;

the actual fiscal impact of proposals,

the distinction between exact levy-neutral and statutorily adjusted “revenue-neutral” calculations,

and the true scale of resulting increases in property tax collections.

When official messaging emphasizes;

reduced nominal tax rates,

and comparisons to statutorily adjusted “revenue-neutral” figures,

without equally prominent disclosure regarding tax increases and spending expansion, taxpayers appear to have been deprived of meaningful understanding necessary for informed public participation and challenge.

The lack of clarity most likely retarded the amount of appeals due by May 15th, which has now passed.

Requested Action

Accordingly, the undersigned respectfully requests;

Review of whether the County’s public presentation of reassessment-era tax increases provided meaningful transparency, meaningful public notice, and meaningful opportunity for informed public participation consistent with the County’s ethical obligations, procedural fairness principles, and the Due Process protections of the 14th Amendment to the United States Constitution;

Review of whether taxpayers were provided sufficiently clear disclosure regarding the true scale of resulting increases in total property tax collections, the distinction between exact levy-neutral calculations and statutorily adjusted “revenue-neutral” calculations, and the extent to which proposed budgets depended upon dramatically increased reassessment-driven revenues;

Review of whether Chairman Alston should have recused himself from matters involving Guilford County Schools appropriations, and systems materially connected to overlapping leadership relationships involving Deena Hayes-Greene and REI-associated initiatives;

Review of whether the overlapping leadership relationships involving the City of Greensboro, the City of High Point, Guilford County Schools, the Continuum of Care structure, REI-associated initiatives, the Museum and associated political organizations create public trust and independence concerns inconsistent with the spirit of the County’s ethics standards;

Review of whether the County’s public presentation of revaluation-era tax increases provided meaningful transparency and meaningful public notice consistent with the County’s ethical obligations and procedural fairness principles;

And consideration of stronger disclosure and recusal standards for commissioners involved in organizations receiving county appropriations or participating in overlapping governance networks connected to county-funded systems.

BTW, Signage for “The Alston Realty Group” advertising office space on the taxpayer funded Museum-connected property;

Respectfully submitted,

George Hartzman

Public Integrity Watch

Related;

Disclaimer; This complaint is based upon publicly available documents, public statements, campaign finance records, governmental budget materials, publicly reported information, and publicly observable institutional relationships as of the date of filing.

The complaint raises questions regarding;

transparency,

ethics,

appearance-of-impropriety concerns,

procedural fairness,

public trust,

and overlapping governmental, nonprofit, political, and institutional relationships.

This complaint does not allege criminal conduct, fraud, corruption, unlawful self-dealing, or statutory ethics violations unless specifically supported by independently verifiable evidence.

References to overlapping leadership structures, associational relationships, political organizations, nonprofit affiliations, or public appropriations are included solely for purposes of analyzing;

public governance,

recusal considerations,

transparency concerns,

institutional independence,

and the appearance of impropriety under the Guilford County Code of Ethics and related public accountability principles.

Any conclusions or interpretations contained herein are expressions of opinion and analysis based upon the presently known facts and publicly available information.

Additional records, disclosures, explanations, or clarifications may materially affect the analysis and conclusions discussed herein.

Unless expressly stated otherwise, this complaint does not allege;

bribery,

fraud,

criminal conspiracy,

unlawful enrichment,

corruption,

or intentional misconduct by any specifically named individual or organization.

The complaint instead raises questions regarding whether the totality of overlapping institutional relationships, reassessment-era fiscal messaging, and public funding structures may undermine public confidence, meaningful public notice, transparency, independence, or the appearance of impartial governmental decision-making.