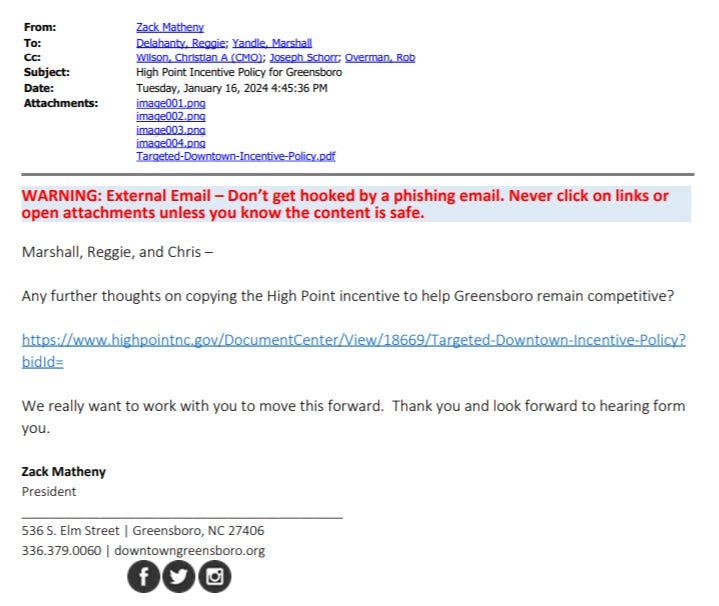

Incentive Push by Greensboro Councilman Matheny Tied to Direct Financial Benefit Through Special Tax District

GREENSBORO, N.C. – Greensboro City Councilman Zack Matheny’s January 16, 2024 push for a new city incentive program was directly linked to a personal financial benefit, an investigation reveals. The nonprofit he leads, Downtown Greensboro Inc. (DGI), is funded not by standard city appropriation but by an extra tax levied on downtown properties. Therefore, any policy that increases downtown property valuations, like the one he advocated for, would directly and automatically increase the budget of the organization he runs and from which he draws a salary.

The Self-Funding Loop

DGI is funded by a Municipal Service District (MSD) tax, a special surcharge on property taxes within a specific geographic area. The revenue from this extra tax is dedicated solely to services within that district, primarily managed by DGI. Therefore, when property values in the downtown MSD rise, or “increase the tax base”, the tax revenue generated for DGI increases, boosting its operational budget.

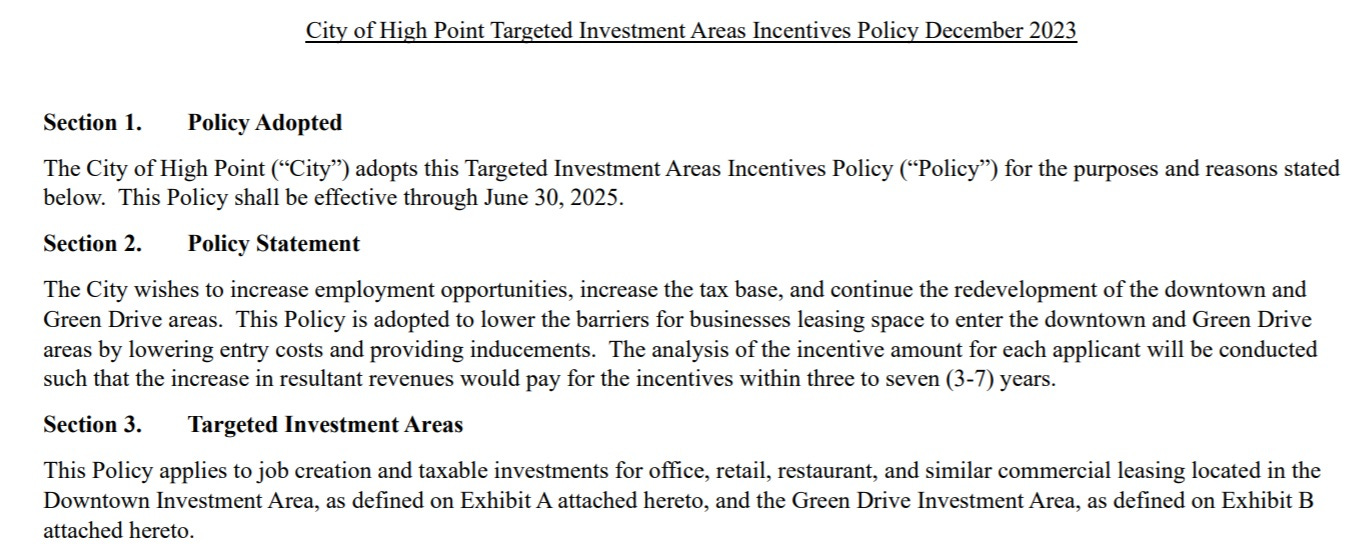

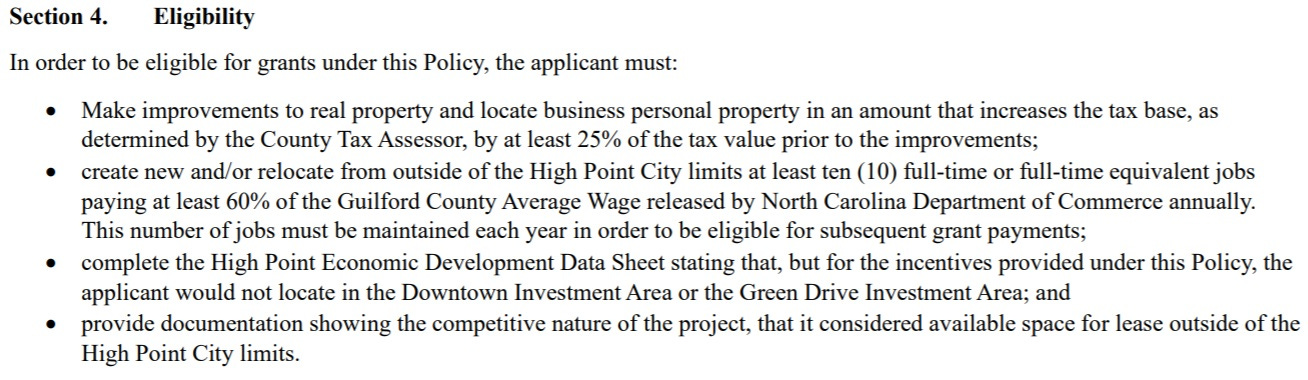

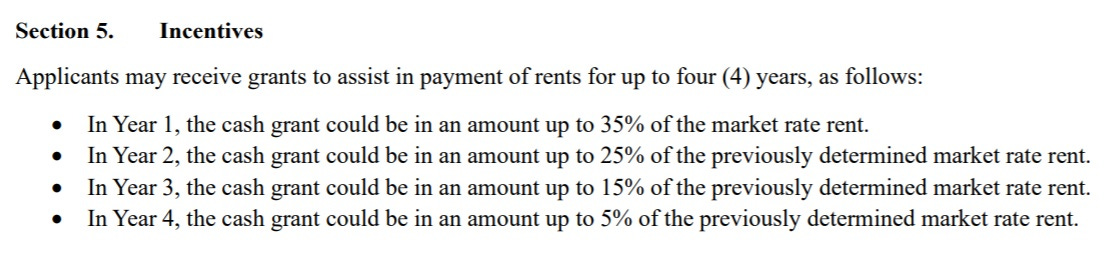

The High Point incentive policy Matheny wanted copied was designed to “increase the tax base” by requiring property improvements boosting tax valuations by at least 25%. If adopted in Greensboro, this would trigger a direct and automatic revenue increase for DGI.

“This isn’t just a conflict; it’s a self-enriching feedback loop,” said a government ethics expert familiar with North Carolina law. “Councilman Matheny proposed a city policy that would use public incentives to increase the value of private property, which in turn increases a special tax, the proceeds of which go to his organization. His advocacy isn’t just for downtown; it’s for the budget of his own nonprofit and, by extension, his own position as its president.”

A Clearer Path to a Statutory Violation

North Carolina General Statute § 14-234.3 prohibits a public official from participating in a contract, “including the award of money,” with a nonprofit they are associated with. Legal analysts state that creating a policy designed to funnel increased tax revenue to one’s own organization falls squarely within the spirit of this law, if not the letter.

“The statute is about preventing a public official from using their office for the financial gain of their associated nonprofit,” the ethics expert explained. “Here, the ‘award of money’ isn’t a one-time grant; it’s a structured, automatic funding stream.

By ‘making’ this policy, Councilman Matheny attempted to directly engineer a financial benefit for DGI. The direct causal chain is undeniable: his policy action leads to increased property values, which leads to more MSD tax revenue for his organization.”

In the wake of Councilman Matheny’s email, city staff had a clear ethical and legal obligation to immediately halt any substantive work on the proposed incentive policy and seek a formal, written opinion from the City Attorney’s office. They should have documented the communication and, in their response to Matheny, politely but firmly stated that due to his direct association with the primary beneficiary nonprofit (DGI) and the clear conflict under N.C.G.S. § 14-234.3, they could not take direction from him on this matter and that all further discussion would require his formal recusal to ensure the process remained lawful and impartial.

DISCLAIMER

The allegations and legal interpretations presented in this article have not been independently verified or adjudicated by any court, ethics board, or regulatory authority. Quotes from unnamed experts cannot be verified. The legal analysis reflects the author’s interpretation of applicable statutes and may differ from official interpretations. The individuals named have not responded to these specific allegations within this article. Readers should consult official records, legal opinions, and statements from all parties before drawing conclusions. This content is for informational purposes only and does not constitute a definitive determination of legal violations or ethical breaches.

Shared..thx!